Iceland's banking system presents a steep learning curve for newcomers. The nation operates on a near-total debit card economy, a reality that confounds many expats. Understanding local card practices is not just about convenience—it directly impacts financial health. This guide explains the system, its hidden costs, and how to navigate it successfully.

The Cashless Reality of Daily Life

Cash transactions now account for less than 10% of all payments in Iceland. From a cup of coffee in Reykjavik's 101 district to ferry tickets in the Westfjords, the debit card is king. Contactless payments dominate, supported by widespread acceptance of mobile wallets like Apple Pay and Google Pay. This shift reflects a broader Nordic trend toward digital finance, rooted in high trust in institutions and universal digital literacy. "We've built an infrastructure where cash is an inconvenience," noted a member of the Althing's Economic Affairs Committee. "The efficiency gains for businesses and consumers are significant."

Icelandic banks issue Visa or Mastercard debit cards linked to domestic accounts. These cards operate on a dual network, functioning both internationally and within Iceland's robust national payment system. This ensures reliability even in remote areas. While foreign cards often work, using them as a primary payment method is where expats encounter unexpected financial pitfalls.

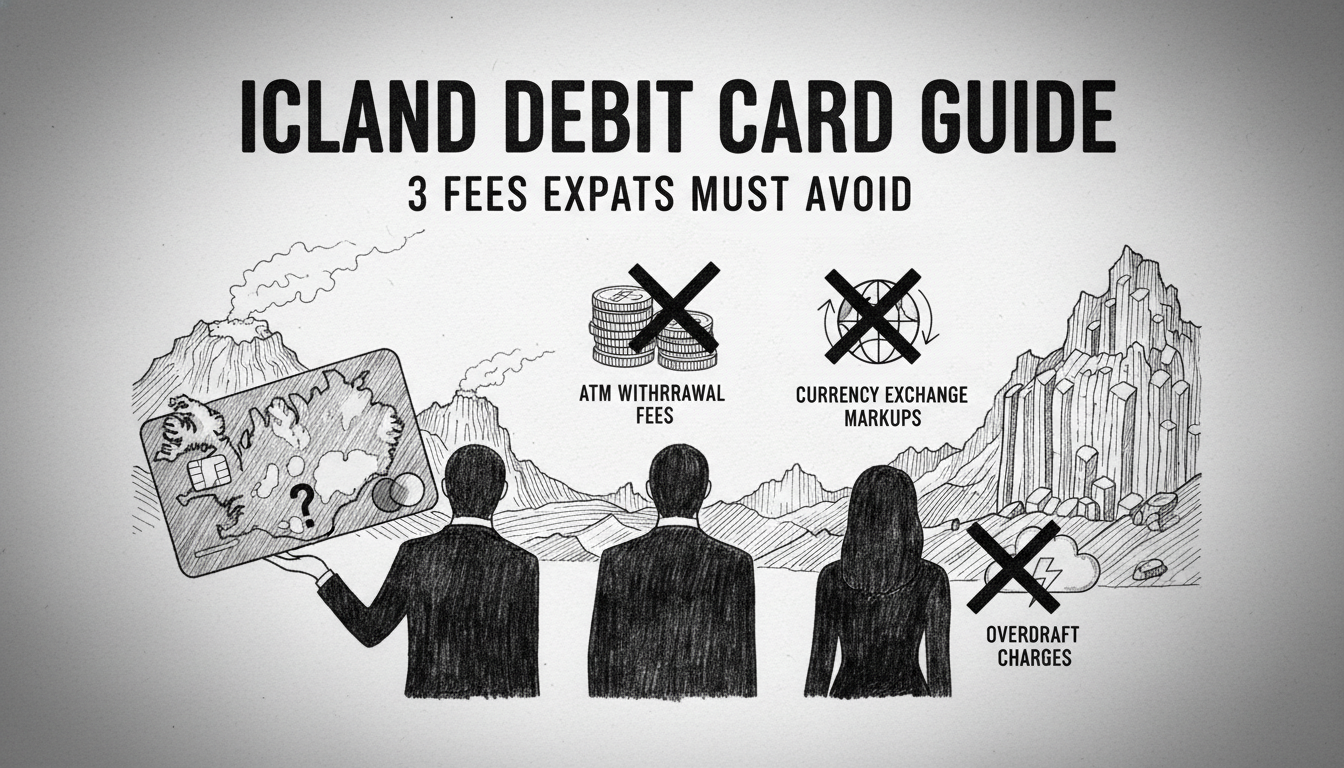

Decoding the Hidden Fee Structure

Foreign debit cards typically trigger two types of fees in Iceland. First, currency conversion fees apply when your home bank converts Icelandic króna (ISK) to your local currency. These fees range from 1% to 3% per transaction. Second, many banks add a separate foreign transaction fee, usually 1% to 2%. Some institutions charge both, silently inflating the cost of every purchase.

Consider a real-world example: an expat buys groceries for 10,000 ISK. If their bank charges a 2.99% conversion fee and a 1.5% foreign transaction fee, the true cost becomes 10,449 ISK. Over months, these micro-charges compound into a significant sum. The average foreign transaction fee from U.S. banks sits between 1% and 3%, making diligent research essential. Financial analysts stress that these fees are the primary budget drain for newcomers unaware of local banking alternatives.

Opening an Icelandic Bank Account: A Step-by-Step Process

For stays beyond a few months, opening a local account is the most cost-effective strategy. The process is straightforward but requires specific documentation. You will need a valid passport, an Icelandic identification number (kennitala) from Registers Iceland, and proof of local address. Banks like Landsbankinn, Arion Bank, and Íslandsbanki typically process applications within five business days.

Choosing a bank often comes down to branch network and digital services. Landsbankinn has 26 branches nationwide, Arion Bank operates 14, and Íslandsbanki maintains 12. All three offer comprehensive English-language online and mobile banking platforms. These apps handle everything from money transfers to setting up automatic bill payments, which is crucial for managing utilities like geothermal heating in Reykjavik apartments. Direct deposit for salaries simplifies compliance and budgeting, integrating expats into the formal financial system.

The Broader Economic Context

Iceland's embrace of digital payments is not accidental. It follows the country's dramatic economic evolution from a fishing-dependent economy to one diversified with tourism, aluminum smelting, and financial services. The 2008 banking collapse led to stringent re-regulation, fostering a secure, transparent, and efficient banking sector. The rapid adoption of cashless technology is a direct outcome of this rebuilt trust and a desire for economic stability.

This system also supports Iceland's environmental goals. Reducing the logistical footprint of cash handling—transportation, security, printing—aligns with national sustainability targets. The efficiency of digital transactions provides clear data for economic planning, from tracking tourist spending in the South Coast to monitoring the financial health of the fishing industry in Akureyri.

Expert Recommendations for New Residents

Financial advisors offer clear guidance for expats. First, contact your home bank before moving to understand all international fee structures. Second, upon arrival, prioritize obtaining your kennitala, as it is the key to all administrative processes. Third, use your foreign card sparingly, only until your local account is active. Withdrawing cash from ATMs should be minimized due to combined fees from both the ATM operator and your home bank.

For daily spending before an account is opened, consider specialized travel cards or credit cards with no foreign transaction fees, though these are not a long-term solution. The ultimate goal is integration into the local system. Icelandic bank accounts offer transparent pricing, with basic accounts often having no monthly fees or domestic transaction charges. ATM withdrawal fees are standardized at around 250 ISK when using another bank's machine.

Navigating a Frictionless Financial Future

Mastering Iceland's debit card system is a fundamental step in successful residency. It moves an expat from being a costly tourist within the economy to an integrated participant. The initial paperwork pays long-term dividends in saved fees, smoother transactions, and financial clarity. As Iceland continues to lead in digital finance within the Nordic region, understanding this landscape is not merely practical—it's essential for anyone building a life on this island. The question for every newcomer is simple: will you pay to learn the system, or will you learn the system to avoid paying?