Denmark's public healthcare system ranks among the world's best. It covers all residents for emergencies and basic care. Yet many expats still consider private health insurance. They seek faster access and broader coverage. This guide examines whether the investment makes sense.

The Public System's Limits

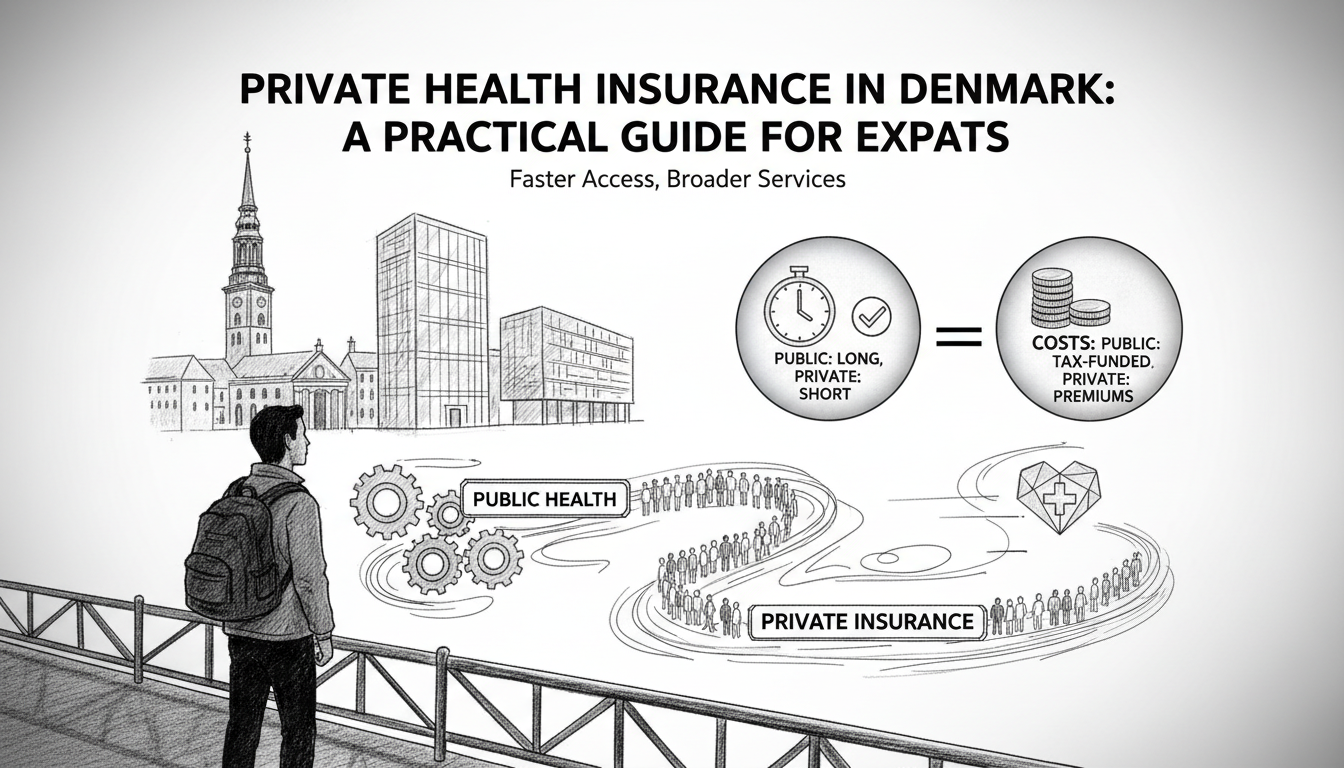

Public healthcare in Denmark operates on a gatekeeper model. Your general practitioner controls specialist referrals. Non-emergency procedures often involve waiting lists. A hip replacement might wait six months. A psychologist appointment could take eight weeks. These delays frustrate newcomers used to immediate care. The system prioritizes medical necessity over convenience.

Private insurance bypasses these queues. It grants direct access to specialists. It covers treatments the public system deems non-essential. Cosmetic dentistry is one example. Physiotherapy beyond basic rehabilitation is another. Many expats value these options. They pay for peace of mind and prompt service.

Tools

Call home for less

Save up to 90% on international calls to family and friends.

Links may be monetized via affiliate partners.

Three Real Insurance Options

Danish insurers offer specific expat products. Topdanmark provides the Expat Health plan. It costs about 500 kroner monthly for a single person. Coverage includes specialist visits without referral. It also pays for alternative medicine like acupuncture. Annual limits reach 100,000 kroner for outpatient care.

Tryg offers the International Health Insurance plan. Premiums start at 600 kroner per month. This plan includes dental coverage up to 5,000 kroner yearly. It also covers mental health services extensively. Many therapists in Copenhagen accept Tryg directly. Patients avoid upfront payments.

Alm. Brand targets expats with its Private Health Extra. The price averages 450 kroner monthly. It focuses on faster diagnostics. MRI scans booked privately happen within days. Public waiting times can exceed three months. The plan also includes travel health insurance abroad. This benefits frequently traveling professionals.

When Insurance Pays Off

Consider Sofia, a software engineer from Canada. She developed chronic back pain last year. Her public doctor prescribed basic exercises. Sofia wanted a specialist consultation immediately. Her Topdanmark policy covered a private orthopedic visit within a week. The specialist recommended advanced physiotherapy. The insurance paid 80% of those costs. Sofia returned to full activity two months faster.

Another case involves David, a British consultant in Copenhagen. He needed extensive dental work. The public system covered only extractions for medical reasons. David's Tryg insurance paid for implants costing 40,000 kroner. He paid just 20% out of pocket. The treatment preserved his dental health long-term.

These examples show tangible benefits. Insurance works best for non-urgent but impactful care. It also helps with preventive services. Regular health screenings often lack public coverage. Private plans include them.

The Cost-Benefit Analysis

Monthly premiums seem modest at 500 kroner. Annual costs total 6,000 kroner. Compare this to potential out-of-pocket expenses. A private psychologist charges 800 kroner per session. Ten sessions cost 8,000 kroner. Dental implants average 25,000 kroner per tooth. Private MRI scans cost 3,000 kroner each.

Insurance makes financial sense for expected needs. Young families might prioritize pediatric coverage. Middle-aged professionals often value musculoskeletal care. Older expats frequently need dental and vision services. Assess your health profile realistically. Then match it to policy specifics.

Consider your Danish residency duration too. Short-term expats benefit most from comprehensive coverage. Long-term residents might integrate into the public system gradually. Many supplement public care with selective private policies. They insure only dental or physiotherapy services.

Practical Steps to Decide

First, register for your yellow health card. This grants access to public healthcare. Do this immediately upon residence registration. Then evaluate your typical medical needs. Review your home country health history. Project potential issues in Denmark's climate.

Next, compare three insurance providers minimum. Use online tools like Samlino.dk. This platform compares Danish health insurance policies. Input your age, health status, and coverage desires. Generate personalized quotes. Contact brokers like Andersen & Martini for expat advice. They explain policy details in English.

Finally, calculate your risk tolerance. Could you pay 20,000 kroner unexpectedly? Would waiting months for treatment disrupt your work? Answer these questions honestly. Then decide on insurance level.

Frequently Asked Questions

What does public healthcare in Denmark actually cover?

The system covers emergencies, hospitalizations, and GP visits. It includes necessary specialist care after referral. Prescription medications receive partial subsidies. Dental care for adults covers only extractions for medical reasons. Basic physiotherapy has limited sessions. Mental health services have long waiting lists.

How much does private health insurance cost for expats?

Premiums range from 400 to 800 kroner monthly. Age and health status affect prices. A 30-year-old non-smoker pays about 500 kroner. A 50-year-old might pay 700 kroner. Family plans cost 1,200 to 2,000 kroner monthly. Deductibles typically range from 1,000 to 5,000 kroner annually.

Can I use private insurance alongside public healthcare?

Yes, most expats use both systems. They visit public hospitals for emergencies. They use private insurance for elective procedures. Some treatments require co-payments even with insurance. Typical co-pay rates are 20% for outpatient care. Always check policy details before treatment.

Which insurance companies are best for English speakers?

Tryg, Topdanmark, and Alm. Brand all offer English service. Their websites provide full information in English. Customer service lines have English-speaking staff. Insurance documents come in English translation. Brokers like Andersen & Martini conduct consultations in English.

How long do I need to wait before insurance coverage begins?

Most policies have a 30-day waiting period. Pre-existing conditions often have longer exclusions. Some insurers exclude them entirely for six months. Always declare medical history accurately. Non-disclosure voids claims later.

Does private insurance help with dental costs in Denmark?

Yes, most plans include dental coverage. Annual limits range from 5,000 to 15,000 kroner. They cover check-ups, fillings, and crowns. Cosmetic procedures like whitening often receive partial coverage. Orthodontics for adults requires special add-ons.

What happens to my insurance if I leave Denmark?

Most Danish policies terminate upon residence cancellation. Some insurers offer portable international plans. These cost significantly more. Consider travel insurance for transition periods. Notify your insurer 30 days before moving.