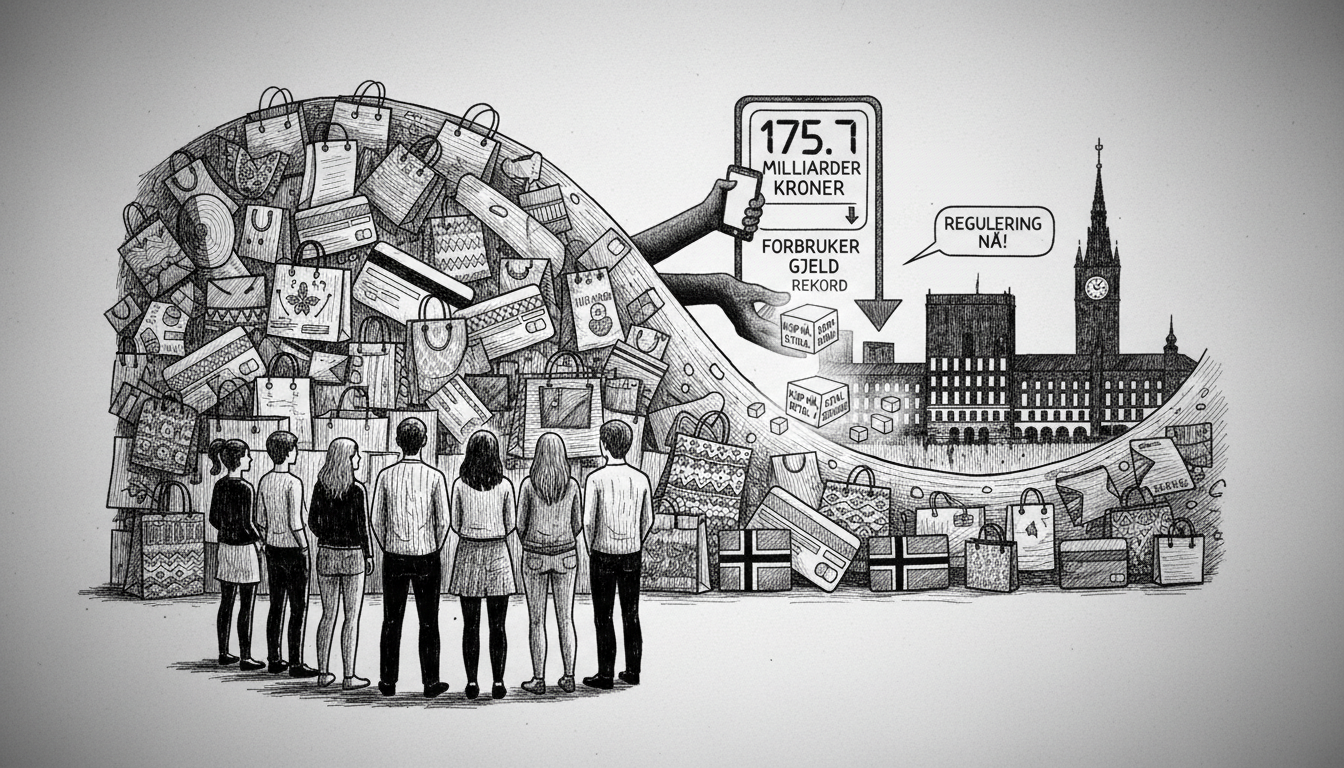

Norwegian households face unprecedented consumer debt levels as shopping promotions create financial pressure. Consumer debt reached 175.7 billion kroner in October, setting a new national record. Experts predict this figure will grow by two to three billion kroner during the current shopping season.

Hege Grønkilen from Løten represents thousands of Norwegians struggling with debt. She accumulated nearly one million kroner through credit cards and buy-now-pay-later schemes. Her experience began with small purchases but escalated during home renovations. The psychological need to fit into society drove her spending patterns, she explained.

Egil Årrestad of Gjeldsregisteret AS monitors unsecured personal debt across Norway. He confirms consumer debt has increased by 4.7 billion kroner this year alone. The growth trajectory shows no signs of slowing, particularly around major shopping events. Buy-now-pay-later services contribute significantly to this expansion, according to debt registry data.

The Consumer Council expresses particular concern about young consumers. Many fail to recognize that deferred payment options constitute actual credit arrangements. Guro Sollien Eriksrud, the council's consumer economics director, notes their unpublished research reveals troubling patterns. One in six users of deferred payment schemes experience negative consequences.

Financial authorities face mounting pressure to address the debt situation. The combination of social media marketing and easy credit access creates perfect conditions for overspending. This trend affects household stability and broader economic indicators. Norway's consumer protection framework faces its most significant test in years.

Klarna, the dominant player in Norway's deferred payment market, faces regulatory scrutiny. The Consumer Council filed a formal complaint alleging inadequate cost disclosure. Company representatives dispute these claims, arguing their marketing materials provide full transparency. They attribute any confusion to outdated physical store signage rather than systemic issues.

Grønkilen's recovery required multiple interventions. She contacted several banks without success before finding assistance through a Facebook seminar. Refinancing through Husbanken combined with guidance from consumer advocates and NAV created her path forward. Her experience underscores the importance of early intervention and financial education.

The Norwegian consumer debt situation reflects broader regional patterns across Nordic countries. Similar trends emerge in Sweden and Denmark, though Norway's oil wealth creates distinct economic dynamics. Policy makers must balance consumer protection with economic growth considerations. This challenge requires coordinated action across government agencies and financial institutions.