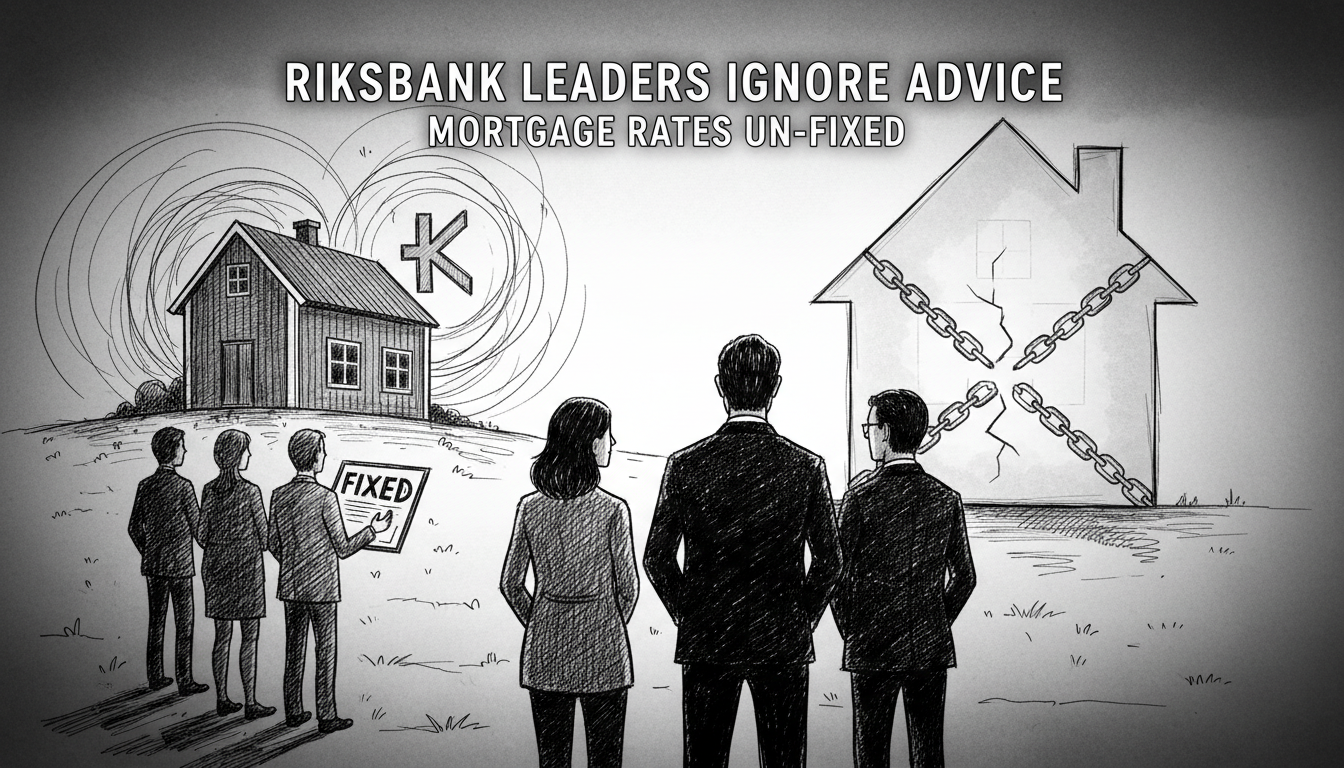

Senior economists across Sweden now advise homeowners to consider fixed-rate mortgages. The governing board of the Riksbank, Sweden's central bank, has chosen a different path. All its top officials maintain variable-rate home loans. This divergence highlights a critical tension in Swedish monetary policy. It also raises questions about policy signals sent from the government district in Stockholm.

The Riksbank's leadership operates from its headquarters near Rosenbad. Its decisions directly influence the Swedish government's broader economic strategy. The bank has aggressively raised interest rates to combat inflation. This policy has sharply increased costs for households with variable-rate mortgages. Many families now face severe financial pressure. Independent analysts and banking economists recently formed a consensus. They suggest the current economic climate favors locking in interest rates.

This council of experts includes chief economists from major financial institutions. They base their advice on forecasts for prolonged inflationary pressure. The Riksbank's executive board, led by Governor Erik Thedéen, has not followed this guidance. All six board members reportedly have variable-rate mortgages on their own homes. This personal financial position is at odds with the expert council's public recommendation.

The situation presents a clear communication challenge for Swedish monetary authorities. Officials at the Riksbank building set policy that affects millions of loans. Their personal financial choices can be seen as a signal of their own confidence. Choosing variable rates suggests they believe inflation will fall quickly. This would allow for future rate cuts. If they are wrong, ordinary Swedes bear the cost of higher, unpredictable payments.

Historical context is important here. The Swedish housing market is highly sensitive to interest rate changes. A large majority of household debt is tied to variable rates. This structure is unique among developed economies. Past Riksdag decisions have shaped this market, often aiming to promote homeownership. The current government policy in Sweden must now manage the fallout from rapid monetary tightening. Many analysts argue the system itself creates excessive risk for the national economy.

This episode goes beyond personal finance for a few officials. It touches on the credibility of Sweden's economic stewardship. The Riksbank's mandate is to ensure price stability. Its tools are interest rates and communication. When its leaders' personal actions contradict widespread expert advice, it muddles their message. It forces the public to guess what the bank truly expects. For international observers, it reveals the complex pressures within Stockholm politics. The Swedish Parliament often debates housing finance, yet concrete protective measures remain elusive.

The immediate implication is continued uncertainty for borrowers. They must decide whether to trust the experts or follow the central bankers' example. The long-term implication concerns institutional trust. Clear, consistent signals are vital for effective economic policy. When actions and words diverge at the highest level, it weakens the policy framework. The coming months will show whose assessment of the economy was correct. The financial well-being of Swedish households hangs in the balance.