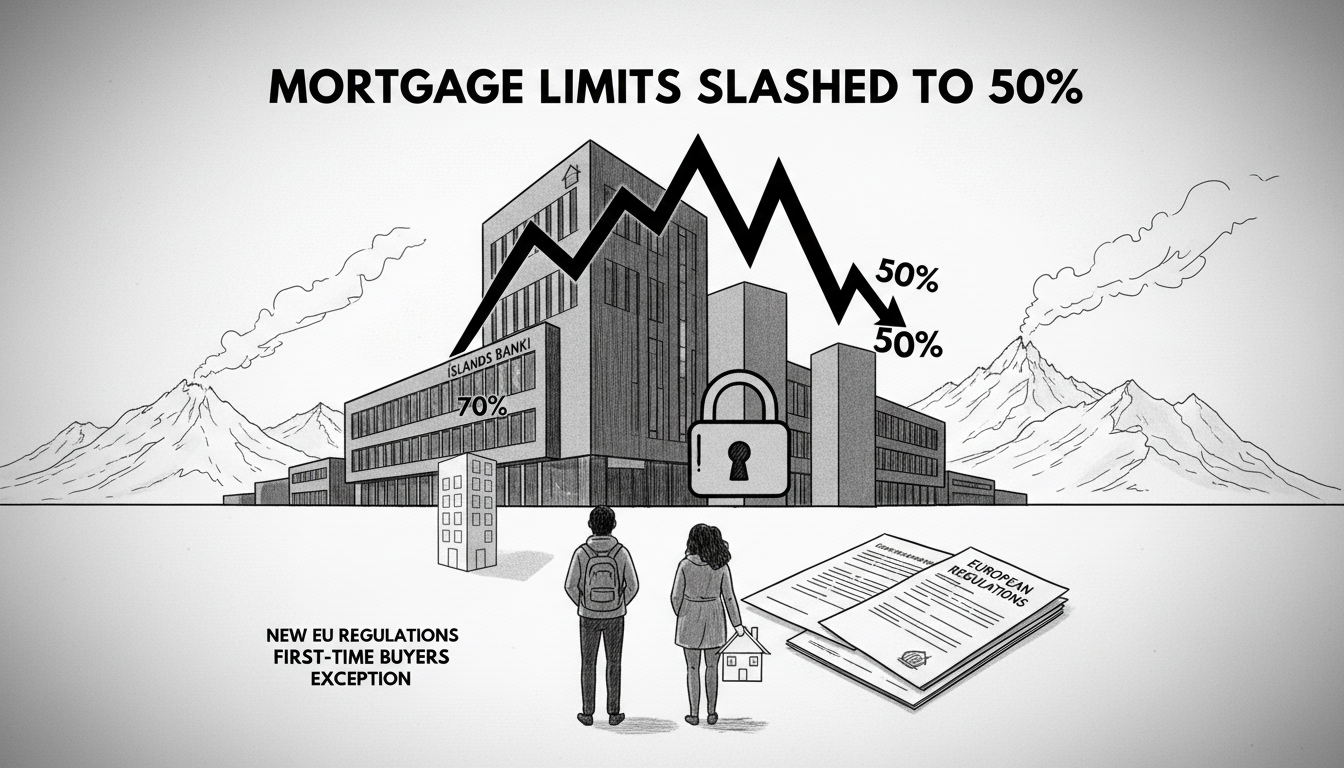

Iceland's banking sector is tightening mortgage rules dramatically. Íslandsbanki now limits core mortgages to just 50% of property purchase prices. The remaining financing falls under supplementary loans with less favorable terms.

The bank confirmed these changes in September. Core mortgages for property purchases now cover 50% of purchase price. Previously they covered 70% of property valuation. This represents a substantial reduction in accessible financing for home buyers.

Supplementary loans now range from 50% to 80% of purchase price. The old system allowed 70% of property valuation up to 80% of purchase price. For refinancing, core mortgages cover 50% of property valuation. Supplementary refinancing loans range from 50% to 70% of valuation.

First-time buyers still qualify for special housing financing. They can access up to 85% of apartment purchase prices. This exception aims to support new entrants to Iceland's challenging housing market.

The changes respond to new capital requirement regulations known as CRR III. European banking authorities are implementing these rules across member states. Icelandic banks must comply with these international standards.

Iceland's housing market faces unique pressures. The country's small population and geographic isolation create supply constraints. Reykjavik's urban concentration drives particular demand pressures. These new lending rules may cool housing demand but could also price out middle-income buyers.

Bank officials stated the adjustments align with regulatory requirements. They emphasize maintaining financial stability in Iceland's banking system. The changes affect both new purchases and existing mortgage refinancing.

What does this mean for average Icelanders? Home ownership becomes more difficult to achieve. Buyers need larger down payments and face higher costs for supplementary financing. The rental market may see increased demand as ownership barriers rise.

The timing raises questions about economic policy priorities. Iceland continues recovering from previous banking crises. Authorities balance financial stability against housing accessibility. These new rules clearly prioritize banking security over housing affordability.

International readers should understand Iceland's context. The nation of 370,000 people maintains strict financial controls since its 2008 crisis. Icelandic banks operate with conservative lending standards compared to other Nordic countries. These latest changes reinforce that cautious approach.

How do Icelandic mortgage rules compare to other countries?

Iceland now has among the strictest mortgage requirements in Europe. Most EU countries allow 80-90% loan-to-value ratios for primary residences. Iceland's 50% core mortgage limit represents extreme conservatism by international standards.

Will other Icelandic banks follow this policy?

Industry analysts expect other major Icelandic banks to adopt similar standards. The regulatory pressure affects all financial institutions. Competitive dynamics typically lead to policy alignment across the banking sector.