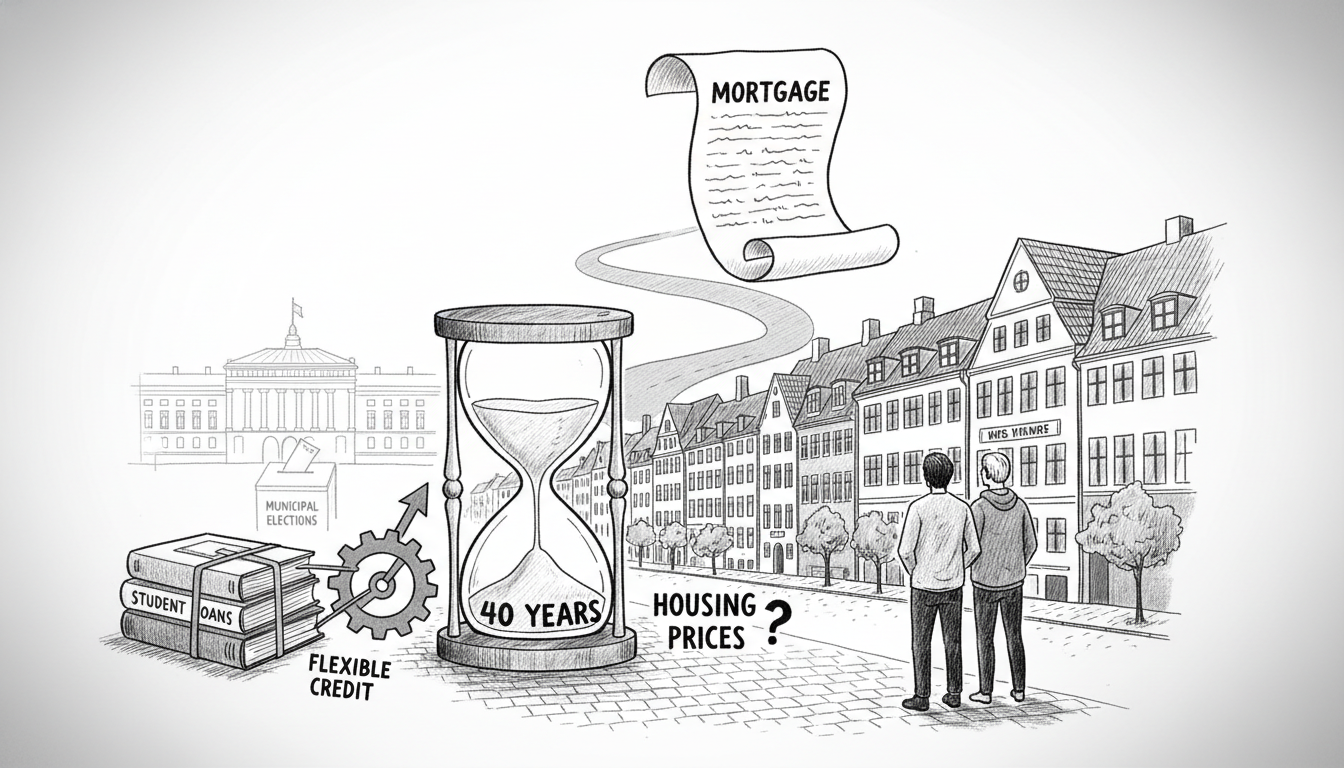

The Danish government wants to make housing more accessible for first-time buyers. New proposals would extend mortgage repayment periods from 30 to 40 years. This change could lower annual payments by approximately 6,700 kroner per million borrowed. That equals about 560 kroner monthly savings for borrowers.

Chief economist Marc Lund Andersen from the Housing Economics Knowledge Center welcomes the intention but questions the long-term effects. He says the measure might help initially but could drive up prices over time. More people would compete for the same limited housing stock, particularly in Copenhagen's tight market.

The proposed 40-year mortgages would allow up to 80% loan-to-value ratios. Current rules limit repayment periods to 30 years maximum. The government also wants longer repayment terms for student loans and more flexible credit assessments.

Andersen notes existing homeowners could also access these new loan options. People who already built housing wealth might bid more aggressively, potentially offsetting benefits for first-time buyers. The economist points out complex dynamics make outcomes difficult to predict precisely.

The proposals arrive during campaign season ahead of municipal elections. They form part of a broader housing package expected soon. The government additionally wants municipalities to require up to 25% owner-occupied homes in new developments.

Andersen expresses skepticism about the ownership requirement. He says forcing specific occupancy types creates legal complications. The only feasible method might involve registering usage restrictions on individual properties. That approach could diminish property values, requiring price discounts for buyers.

Copenhagen's housing shortage remains acute despite various government interventions. The city faces intense competition for relatively few available homes. Previous measures have struggled to balance accessibility with market stability.

These proposals represent the latest attempt to address Denmark's persistent housing challenges. Similar initiatives in other Nordic countries have produced mixed results. Sweden and Norway also grapple with balancing market access and price stability in major urban centers.

The timing suggests political considerations alongside policy objectives. Housing affordability consistently ranks among top voter concerns in Danish elections. The coming weeks will show whether these measures gain traction or face opposition.